U.S. stocks posted gains for the week, led higher by technology and energy shares. The Dow Jones Industrial Average advanced 121 points to 25,790, a gain of 0.5%.

U.S. Markets: The technology-heavy NASDAQ Composite added 130 points or 1.7% to close at 7,945. By market cap, smaller cap indexes outperformed large caps. The large cap S&P 500 added 0.9% while the mid cap S&P 400 and small cap Russell 2000 added 1.2% and 1.9% respectively.

International Markets: Canada’s TSX and the United Kingdom’s FTSE were the laggards among major international markets, rising 0.2% and 0.3% respectively. On Europe’s mainland all larger markets finished the week in the green with France’s CAC 40 up 1.6%, Germany’s DAX up 1.5%, and Italy’s Milan FTSE up 1.6%. Asian markets were similarly higher - China’s Shanghai Composite added 2.3%, while Japan’s Nikkei added 1.5% and Hong Kong’s Hang Seng added 1.7%. As grouped by Morgan Stanley Capital International, emerging markets added 2.8% and developed markets were up 1.4%.

Commodities: Precious metals recovered much of last week’s plunge as Gold added 2.5% or $29.10 to end the week at $1213.30 per ounce, and Silver added 1.1% to end the week at $14.79 per ounce. Crude oil surged 5.4% to close at $68.72 per barrel of West Texas Intermediate. The industrial metal copper - sometimes referred to as “Dr. Copper” for its ability to forecast global economic growth - rebounded 2.7% after 3 weeks of negative returns.

U.S. Economic News: The labor market remains very tight as new claims for unemployment benefits fell by 2,000 to 210,000 nearly matching its lowest level since December of 1969. Economists had expected a rise to 215,000 claims. The current decline in new claims is the third lowest reading during the current nine-year-old economic expansion, just 2,000 above the post-recession low set in July. The four week average of claims, smoothed to iron out the weekly volatility, fell by 1,750 to 213,750, also near its lowest level since 1969. The number of people already collecting unemployment benefits, known as continuing claims, remained barely changed at 1.73 million.

The number of existing homes sold in July fell for a fourth consecutive month as a shortage of properties on the market and rising mortgage rates are thought to have sidelined some potential buyers.

Sales of new homes also declined – again - falling 1.7% in July, the third decline in the past four months. The Commerce Department reported new home sales ran at a 627,000 annualized rate, the lowest level in nine months. The reading widely missed economists’ forecasts for a gain of 2.2%.

A big drop in new contracts for passenger jets caused orders for durable goods to fall 1.7% last month, its third decline in the past four months and the most since the beginning of the year. Economists had forecast a 1.1% decline.

An index that tracks U.S. manufacturers and service-oriented companies showed slower growth this month, suggesting that economic growth may be tapering from its three-year peak this spring. Research firm IHS Markit’s flash Purchasing Managers Index (PMI) manufacturing sub-index fell to a nine-month low of 54.5 from 55.3, while its services sub-index hit a four-month low of 55.2, down 0.8 point.

Minutes of the Federal Reserve’s meeting earlier this month signaled broad support for another interest-rate hike in September if the data continued to support their outlook. The minutes said, “It would likely soon be appropriate to take another step in removing policy accommodation.” However, officials cautioned that it may have to pause its gradual rate hike path if international trade tensions continued to escalate. Fed officials were unanimous in their view that trade disagreements represented a downside risk to the economy. Fed officials also agreed they would "fairly soon" need to scrap the language describing their policy stance as "accommodative" because the level of rates is getting closer to neutral.

International Economic News:

The European press has shown very little sympathy for the ‘no-deal’ Brexit guidance published by UK Brexit Secretary Dominic Raab. The German press provided the most coverage of Raab’s publication with most papers summarizing Raab’s writings as “too little, too late”. The prevailing feeling on the European continent is that “it is the Brits’ own damn fault” for the current chaos and uncertainty. Journalist Stephanie Bolzen said in a column for the German conservative daily Die Welt that “this attitude is arrogant” and “detrimental”. If a no-deal Brexit leads to the end of the free market this will create “shock waves well beyond Europe”, she wrote.

Business morale in France fell to its lowest level since Emmanuel Macron became the President in May 2017, French statistics agency INSEE reported. Sentiment soared following Macron’s election promising investor-friendly reforms and a return to fiscal discipline, but has soured since then. The composite business morale index dropped to 105 in August, down almost 6 points from its multi-year high last year. INSEE gave no reason for August's decline, though respondents in recent business surveys have cited uncertain trade prospects and rising energy prices as negatives. On a positive note, the latest reading still remains above the long-term average of 100.

Strong domestic demand drove Germany’s economic expansion in the months leading up to summer as second quarter gross domestic product rose 0.5%, matching estimates. Overall economic growth was supported by a 0.5% increase in capital investment, mostly due to construction. Net trade, however, weighed as imports rose 1.7% but exports were up just 0.7%. The country’s solid performance in the second quarter helped alleviate concerns that slowdown in the first quarter would persist. Nonetheless, several large corporations in Germany expressed concern over the outlook, with growth in China slowing and emerging markets experiencing a slowdown. The Bundesbank stated German expansion is likely to cool this quarter, though the economy remains on a “sound growth path”.

Analysts note that China’s economy is slowing down, but they debate about how much trouble it is really in. The recent weakness appears at least partly due to a budding trade war with the United States, in which each country has imposed tariffs of $50 billion on each other’s goods and each are threatening far more. While China’s economy expanded 6.9% in 2017 according to government figures, official data showed a slowdown in investment, factory production and retail sales in July. Chang Liu, China economist at Capital Economics wrote in a note to clients, “The US-China trade conflict will be a drag on activity, though probably a small one. Instead, we expect the economy to weaken mainly due to domestic headwinds caused by slower credit growth.” Some experts feel that the slowdown fears are overblown. Doug Morton, head of Asia research at Northern Trust Capital Markets, pointed out that some indicators like demand for oil and the property markets are still strong. "Headlines on growth concerns may prove to be somewhat exaggerated," he wrote in a note to clients this week.

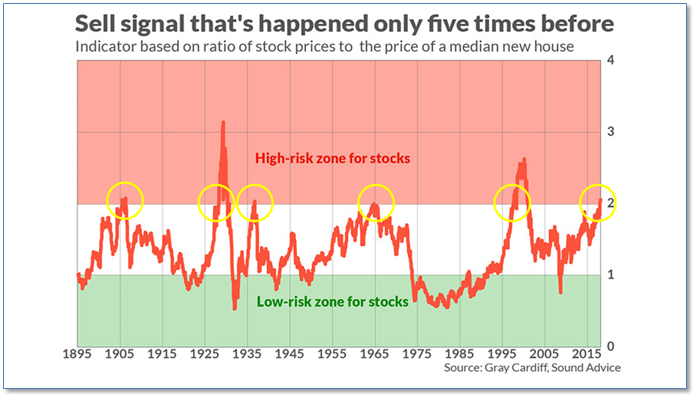

Finally: As the bull market continues through its ninth year, a little-known stock market indicator with a “5 for 5” record since 1895 has just generated a sell signal. The indicator is the creation of Gray Cardiff, editor of the Sound Advice newsletter. He calls it the “Sound Advice Risk Indicator”, which is simply the ratio of the S&P 500 to the median price of a new home. Cardiff explains that the indicator quantifies the “struggle for capital” between stocks and real estate. When the indicator rises above 2.0, he explains, it means the stock market has absorbed a “larger proportion of available investment capital than economic conditions can justify.” The last time the indicator flashed a sell signal was in 1998—conveniently before the dot.com implosion that followed. Note, however, that this indicator did NOT give a sell signal in 2007, since it was Real Estate that had proportionately too much investment then!

- Please visit our website www.pacificinvestmentresearch.com for more insights. Email us at info@pacificinvestmentresearch.com if you have any questions.