In the markets:

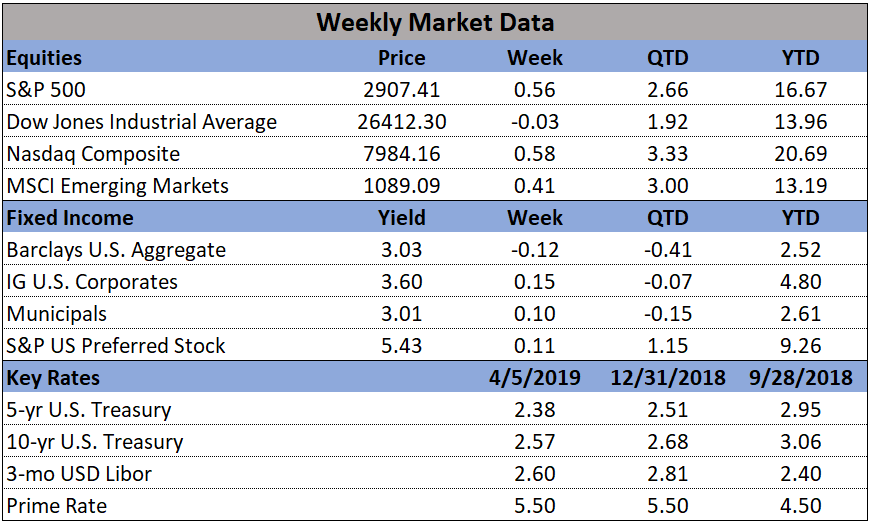

U.S. Markets: Most of the major U.S. indexes recorded small gains for the week. Trading volumes, however, were notably lower with daily volumes hitting new year-to-date lows on Monday, Wednesday, and Thursday of the week. The narrowly-focused Dow Jones Industrial Average ended the week down 12 points, or -0.05%, to close at 26,412. The technology-heavy NASDAQ Composite gained 0.6% and neared the 8000-level, closing at 7,984. By market cap, the large cap S&P 500 index gained 0.5% for the week (and in the process moved within roughly 1% of its all-time high established in September 2018), while the S&P 400 mid cap index rose 0.9% and the small cap Russell 2000 gained a lesser 0.1%.

International Markets: Canada’s TSX rose 0.5%, while the United Kingdom’s FTSE retreated -0.13%. On Europe’s mainland, France’s CAC 40 rose 0.5%, but Germany’s DAX retreated -0.08%. Italy’s Milan FTSE also gained 0.5%. In Asia, China’s Shanghai Composite retreated -1.8% following last week’s big 5% surge. Japan’s Nikkei tacked on an additional 0.3% to last week’s gain. As grouped by Morgan Stanley Capital International, developed markets rose 0.3%, while emerging markets were off -0.1%.

Commodities: Precious metals finished the week down slightly. Gold ticked down $-0.40 to $1295.20 an ounce, while Silver dipped -0.8% to $14.96. Energy continued to rally, now up 6 weeks in a row. West Texas Intermediate crude gained 1.3%, finishing the week at $63.89 per barrel. The industrial metal copper, viewed by analysts as a barometer of global economic health due to its variety of uses, retraced all of last week’s decline and then some by rising 1.8%.

U.S. Economic News: For the first time in 50 years, the number of claims for first-time unemployment benefits fell below 200,000. The Labor Department reported the number of new jobless claims fell by 8,000 to just 196,000 last week. Economists had expected a reading of 210,000. Jobless claims have fallen four weeks in a row, just a few months after hitting a short-term high of 244,000. The monthly average of claims, smoothed to iron out the weekly volatility, declined by 7,000 to 207,000. That number was also near its lowest level since 1969. Continuing claims, which counts the number of people already receiving benefits, fell by 13,000 to 1.71 million.

The amusingly-named JOLTS report (Job Openings and Labor Turnover Survey) showed the number of job openings across the country fell to its lowest level in nearly a year, said the Labor Department. Job openings fell by more than half a million to 7.1 million in February, its lowest level since March 2018. The U.S. added only 33,000 new jobs, the smallest increase in a year and a half. Economists blamed a severe cold spell, the residual effects of the government shutdown and other seasonal disruptions for the unusually small gain. However, even after the significant drop there still remain almost 800,000 more open jobs available than the number of Americans officially classified as unemployed. The closely watched “quits rate” part of the JOLTS report remained at 2.3% for the ninth month in a row. The quits rate gives an underlying view of the strength of the labor market as it is presumed that an employee would most likely only leave a position if he or she had a high confidence in finding another, more lucrative one. The current rate is the second-highest it’s been since the government began keeping track in 2000.

Sentiment among the nation’s small business owners ticked up in March, remaining at a historically strong level. The National Federation of Independent Business (NFIB) reported its Small Business Optimism Index increased 0.1 point to 101.8. The reading marked the third month in a row remaining at or near its highs. In the details, 23% of business owners surveyed by NFIB said the next three months was a good time to expand, a point higher than last month. In addition, 60% reported hiring or trying to hire new employees, but 54% reported few or no qualified applicants for the positions they were trying to fill. Over 20% cited the difficulty of finding qualified workers as their Single Most Important Business Problem—just 4 points below the record high.

Consumers paid more for gas and rent last month, but broader inflationary pressures remained contained, according to the Bureau of Labor Statistics. The government reported the Consumer Price Index (CPI) jumped 0.4% in March, the biggest increase in over a year. The reading matched economists’ forecasts. Over the past year, the cost of living has increased 1.9%, up from 1.5% in February. The majority of the increase in March was due to higher energy prices. Stripping out the volatile food and energy categories, so-called “core” CPI was up just 0.1%. Furthermore, the annual core CPI slipped to 2% from 2.1%. That’s the lowest level in a year.

At the producer level, wholesale prices surged due to the higher cost of energy, but overall inflation remained tame. The Bureau of Labor Statistics reported its Producer Price Index (PPI) climbed 0.6% last month. Economists had expected just a 0.3% increase. Almost all of the increase was due to the higher cost of gas. Stripping out food and energy prices, core PPI was flat for the month. The rate of wholesale inflation over the past 12 months rose 0.3% to 2.2% in March, but that remained far below the seven-year high last summer of 3.4%. The reading reinforces the belief that significant inflation isn’t on the horizon, at least not yet. Economists Gregory Daco and Jake McRobie of Oxford Economics told clients in a note, “We believe this tame inflationary environment continues to provide the Fed with reason to remain patient as it assesses economic and inflation conditions.”

The Federal Reserve’s decision last month to cease raising interest rates this year was driven by concerns over the U.S. and global economies and surprisingly tame domestic inflation data, Fed meeting minutes showed. Last month the Fed aborted plans to keep raising key short-term interest rates, with Chairman Jerome Powell stating the Fed would remain “patient”. On the Fed’s list of worries: sluggish U.S. growth early in the new year, a weaker global economy, the messy attempt by the U.K. to leave the European Union and festering trade tensions between the Trump administration and China. “A majority of participants expected that the evolution of the economic outlook and risks to the outlook would likely warrant leaving the target range unchanged for the remainder of the year,” the minutes said. With regards to inflation, the Fed stated, “It was noteworthy that [inflation] had not shown greater signs of firming in response to strong labor market conditions and rising nominal wage growth, as well as to the short-term upward pressure to prices arising from tariff increases.”

Looking ahead:

It's a slow week heading into the Easter weekend. Markets will be closed Friday, and most economic reports set to be released this week are lower-tier. That said, there is still plenty to watch.

Here's what PIR will be monitoring this week:

- April 15: Treasury TIC Report, Chicago Fed's Charles Evans speaks in New York

- April 16: Industrial Production Numbers, NAHB Housing Index, Dallas Fed's Robert Kaplan

- April 17: MBA Mortgage Applications, Trade Balance, Wholesale Inventories, Fed's Beige Book

- April 18: Retail Sales, Initial Jobless Claims, Bloomberg Consumer Comfort, Markit PMI

- April 19: Housing Starts, # of Building Permits for March