In the markets:

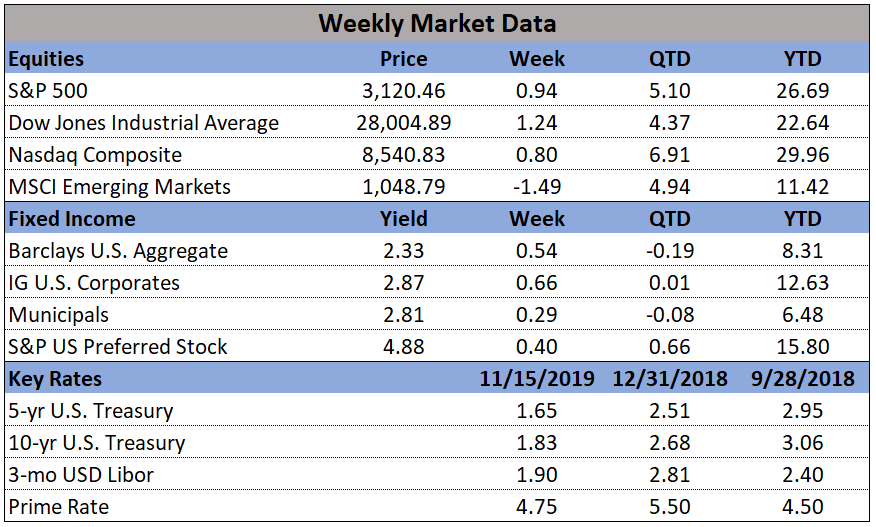

U.S. Markets: The majority of U.S. indexes ended the week higher as investors continued to look for any indication of progress in U.S.-China trade negotiations. The Dow Jones Industrial Average and large cap S&P 500 index, as well as the technology-heavy NASDAQ Composite all established record highs. The smaller-cap benchmarks lagged and ended the week mixed. The Dow rallied 323 points to close at 28,004, a gain of 1.2%. The NASDAQ added 0.8% ending the week at 8,540. By market cap, the large cap S&P 500 gained 0.9% and the mid cap S&P 400 added 0.1%, but the small cap Russell 2000 declined -0.2%.

International Markets: Canada’s TSX rose for a fourth consecutive week, adding 0.9%, while the United Kingdom’s FTSE retreated -0.8%. On Europe’s mainland, France’s CAC 40 rose 0.8%, Germany’s DAX gained 0.1%, and Italy’s Milan FTSE added 0.2%. In Asia, China’s Shanghai Composite dropped -2.5% and Japan’s Nikkei gave up -0.4%. As grouped by Morgan Stanley Capital International, developed markets finished down -1.3%, while emerging markets ticked down -0.1%.

Commodities: Precious metals retraced some of last week’s plunge. Gold rose $5.60 to $1468.50 an ounce, a gain of 0.4%, and silver recovered 0.7% to finish the week at $16.95 an ounce. Oil rose for a second consecutive week. West Texas Intermediate crude oil gained 0.8% to $57.72 per barrel. The industrial metal copper, viewed by some analysts as a barometer or world economic health due to its variety of uses, retreated -1.6%.

U.S. Economic News: The number of Americans seeking first-time unemployment benefits jumped to a nearly 5-month high last week, the Labor Department reported. Initial jobless claims rose 14,000 to a seasonally-adjusted 225,000 last week, the government said. Economists had estimated new claims would total only 215,000. The less-volatile monthly average of new claims rose a much smaller 1,750 to 217,000. The four-week average gives a more stable view of the labor market than the weekly number. Most analysts view the increase as an anomaly in the Labor Department’s seasonal adjustment calculations. Scott Brown chief economist at Raymond James wrote in a research note, “Jobless claims rose more than anticipated, but that’s just seasonal noise (the trend remains low).” Continuing claims, which counts the number of Americans already receiving unemployment benefits, fell by 10,000 to 1.68 million. That number remains near its lowest level since 1970.

The Commerce Department reported that sales at U.S. retailers rebounded last month, but the pace of spending appears to have slowed since the beginning of the year. Retail sales increased 0.3% last month, matching economists’ forecasts. Car dealers, gas stations, and internet stores reaped most of the gains. Most other retailers posted soft results just before the start of the holiday shopping season. Excluding the auto and gasoline categories, sales were up just 0.1%. Furthermore, the pace of sales over the past 12 months has slowed to 3.1% in October, down from 4.1%--a five month low. Still, given the strongest labor market in decades, Americans appear to be in a good position to spend during the upcoming holiday season. Given that household spending accounts for 70% of U.S. economic activity, consumer spending is essential to keep the U.S. economy out of recession.

U.S. consumers paid higher prices for gasoline, vehicles, medical care, and recreation last month according to the Bureau of Labor Statistics, but overall inflation remained low and fairly stable. The Consumer Price Index jumped 0.4% in October, with fuel costs accounting for more than half of the increase. Economists had expected only a 0.3% advance. Over the past year, the cost of living has increased 1.8%--still well below last year’s peak of 3% and just shy of the Federal Reserve’s target of 2%. The measure that strips out the volatile food and energy categories, so-called “core inflation”, ticked down from 2.4% to 2.3%. The relatively low rate of inflation has given the Federal Reserve leeway to cut interest rates to extend the economic expansion entering its 11th year.

At the wholesale level, the cost of goods and services posted their sharpest increase in half a year last month. However, almost all of the gain was due to higher gasoline prices. The Bureau of Labor Statistics reported its producer price index rose 0.4% last month, 0.1% higher than the estimate of economists. More broadly, however, producer prices continued to recede. The 12-month rate of wholesale inflation fell to a three-year low of 1.1% from 1.4%. The yearly rate was as high as 3.4% just eighteen months ago. Core PPI, that strips out food and energy was up just 0.1% last month. The 12-month core rate slowed to 1.5% from 1.7%--also a three-year low. Andrew Hunter, senior economist at Capital Economics wrote, “Overall, this all supports our view that there is little danger of inflation rising sustainably above the Fed’s [2%] target. In that environment, interest rates are likely to remain on hold for the foreseeable future.”

Absent a material deterioration in the economy, Federal Reserve Chairman Jerome Powell stated interest rate changes will be on hold for the foreseeable future. In remarks to the Joint Economic Committee of Congress Powell stated, “We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook of moderate economic growth, a strong labor market, and inflation near our symmetric 2% objective.” The Fed has cut interest rates in three quarter-point moves since July, putting the Fed’s benchmark federal funds rate in a range of 1.5%-2%. In further testimony, Powell noted that weakness in the manufacturing sector has not spilled over into the broader economy. The Fed chairman said the economy is being driven by the consumer. “The 70% of the economy that is the consumer’s is healthy, with high confidence, low unemployment, wages moving up,” he said.

In the New York region, manufacturing activity remained sluggish for a sixth consecutive month according to the New York Federal Reserve. The New York Fed’s Empire State business conditions index fell 1.8 points to 1.1 in November. Economists had expected a reading of 5.0. In the details of the report, the new orders index ticked up 2 points to 5.5, while the shipments index fell 4 points to 8.8. Inventories declined and optimism about conditions six months from now remained subdued. Manufacturing in the U.S. has been hit by the trade dispute with China, a relatively strong U.S. dollar making U.S. goods more expensive overseas, and an overall slowdown in global economic growth.