In the markets:

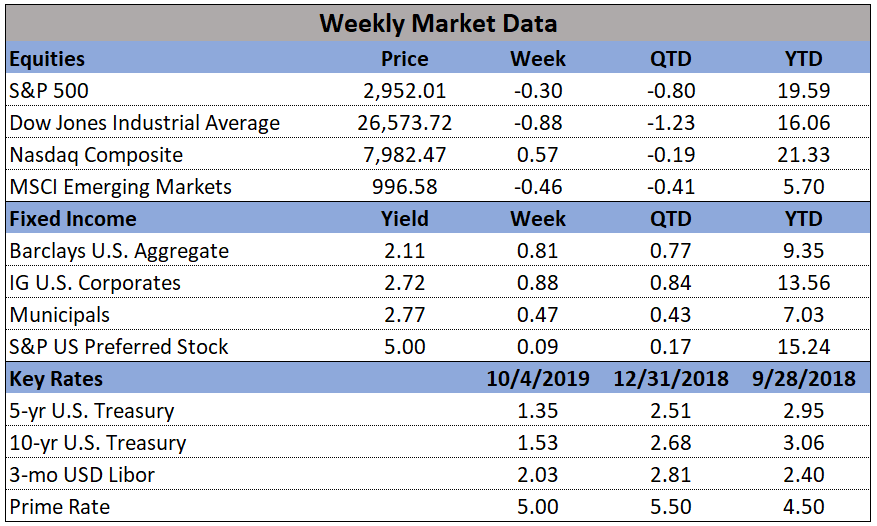

U.S. Markets: Most of the major U.S. indexes suffered their third consecutive week of losses as evidence accumulated of a global economic slowdown. Strength in Apple and other information technology shares supported the NASDAQ Composite, which ended modestly higher for the week and was the lone gainer. The Dow Jones Industrial Average retreated -0.9% ending the week at 26,573. The technology-heavy NASDAQ Composite managed a 0.5% gain for the week. Small caps continued to sell off with the Russell 2000 index falling a further -1.3%, while the S&P 400 midcap index and S&P 500 large cap index retreated -1% and -0.3%, respectively.

For the month of September, U.S. indexes were all positive, but the quarter was mixed with 3 of the “big 5” down for the quarter. Year to date, NASDAQ leads and Small Caps bring up the rear, but all are having a decent year.

|

Index |

September % |

3rd Qtr % |

Year-to-Date % |

|

NASDAQ |

0.5 |

-0.1 |

20.6 |

|

Dow 30 |

1.9 |

1.2 |

15.4 |

|

Mid Cap |

2.9 |

-0.5 |

16.4 |

|

Small Cap |

1.9 |

-2.8 |

13.0 |

|

S&P 500 |

1.7 |

1.2 |

18.7 |

International Markets: Major developed international markets were a sea of red for the week. Canada’s TSX had its second consecutive week of losses giving up -1.5%, while the United Kingdom’s FTSE retraced all of last week’s gain and then some falling -3.7%. On Europe’s mainland, France’s CAC 40 retreated -2.7%, Germany’s DAX fell -3.0%, and Italy’s Milan FTSE gave up -2.5%. In Asia, China’s Shanghai Composite was closed for the week for its National Day holiday. Japan’s Nikkei ended down -2.1%. As grouped by Morgan Stanley Capital International emerging markets rebounded 0.8%, while developed markets ended down -1.2%.

For the month of September, major international indexes were all positive with Japan highest and China lowest, and most were also up for the quarter. Year to date, Italy and France are leading among those shown in the table while Japan is at the rear. What the table doesn’t show is the underperformance in a variety of emerging markets around the world in the third quarter, resulting in the Emerging Markets category being far behind Developed Markets year to date.

|

Index |

September % |

3rd Qtr % |

Year-to-Date % |

|

CAC 40 Index (France) |

3.6 |

2.5 |

20.0 |

|

DAX (Germany) |

4.1 |

0.2 |

17.7 |

|

FTSE 100 (UK) |

2.8 |

-0.2 |

10.1 |

|

FTSE MIB (Italy) |

3.7 |

4.1 |

20.6 |

|

Nikkei 225 (Japan) |

5.1 |

2.3 |

8.7 |

|

TSX (Canada) |

1.3 |

1.7 |

16.3 |

|

Shanghai Exchange (China) |

0.7 |

-2.5 |

16.5 |

|

iShares MSCI Emerging Mkts ETF (EEM) |

1.7 |

-4.8 |

5.4 |

|

iShares MSCI Developed Mkts ETF (EFA) |

3.2 |

-0.8 |

13.3 |

Commodities: Precious metals finished the week mixed. Gold rose 0.4%, ending the week at $1512.90 per ounce. Silver, however, gave up -0.2% closing at $17.62 per ounce. Oil fell back to its August lows, falling -5.5%, to $52.81 per barrel of West Texas Intermediate crude oil. The industrial metal copper, viewed by some analysts as a barometer of global economic health due to its variety of uses, finished the week down -1.4%.

For the month of September, the commodities shown in the table were mixed, but gold and silver nonetheless had a nice third quarter. Year to date, gold and silver lead the group, but copper has languished far behind, perhaps reflecting worldwide economic unease.

|

September % |

3rd Qtr % |

Year-to-Date % |

|

|

Gold (GLD) |

-3.4 |

4.3 |

15.0 |

|

Silver (SLV) |

-7.2 |

11.1 |

9.6 |

|

Oil (XLE) |

3.9 |

-6.2 |

6.0 |

|

Copper (CPER) |

0.8 |

-4.9 |

-1.9 |

U.S. Economic News: The number of people seeking first-time unemployment benefits rose to a one-month high last week, the Labor Department reported. Initial jobless claims rose by 4,000 to 219,000 last week, partially due to the three-week-old labor strike at General Motors that has idled tens of thousands of workers. Economists had forecast a reading of 218,000. Raw or actual claims — before seasonal adjustments — surged in Ohio and remained elevated in Michigan, two states with large auto industries. Some 250,000 workers at GM and some of its parts suppliers have been sidelined during the strike. The less-volatile monthly average of new claims remained unchanged at 212,500. The monthly number usually gives a more accurate read into labor-market conditions than the more volatile weekly number. Continuing claims, which counts the number of people already receiving benefits, declined by 5,000 to 1.65 million. That number remains near a cycle low.

The labor market continues to show resilience in the face of weakening global economic data. The Bureau of Labor Statistics reported the economy added 136,000 new jobs in September, raising hopes that the economy might avoid a recession. Hiring in education and health services led the way, followed by professional and business services. Retail trade suffered the worst pullback. Economists had forecast an increase of 150,000. The reading was the slowest pace of job growth in four months, but employment gains for August and July were revised up by a combined 45,000. To put the reading into perspective, the pace of job growth has slowed from 223,000 per month in 2018 to 158,000 over the last three months. In a separate survey, the U.S. unemployment rate dropped to just 3.5%--its lowest rate since December 1969. However, one concern in the report was worker pay. The annual rate of increase in compensation fell to 2.9% from 3.2%.

Manufacturing activity in the Windy City contracted for the third time in four months, according to research firm MNI Indicators. MNI reported their Chicago Purchasing Managers Index (PMI) business barometer dropped to 47.1 in September, down from 50.4 in August. Readings below 50 indicate worsening conditions. Economists had expected a reading of 50. The details of the report show widespread weakness. Production in the Chicago region hit a 10-year low, exaggerated by the UAW strike at GM. However, unrelated to the strike, the report also showed declines in orders and inventories. MNI notes that the eroding business conditions in the Chicago region mirror the nationwide trend in manufacturing. A stronger U.S. dollar, slowing global economy, and ongoing trade dispute between the U.S. and China have all curbed demand for U.S. manufactured goods.

Nationwide, manufacturers experienced their worst month since the 2007-2009 Great Recession according to the Institute for Supply Management (ISM). ISM reported its manufacturing index plunged deeper into contraction to 47.8 last in September, down from 49.1. The reading marks its lowest level since June of 2009. Economists had expected the index to rebound to 50.2. In the details of the report, production, employment, and inventories all declined. New orders did tick up, but remained in contraction at 47.3—its weakest level in a decade. Furthermore, only three of the eighteen U.S. manufacturing industries tracked by ISM reported growth, down from nine in the prior month. Chris Low, Senior Economist at FTN Financial wrote in a research note, “Manufacturing weakness is close to dangerous levels. Historically, readings under 46 are consistent with recession.”

The services sector, which makes up almost 80% of U.S. GDP, registered its weakest growth in September in more than three years, according to the Institute for Supply Management (ISM). ISM’s non-manufacturing index fell to 52.6 last month, down 3.8 points from August. The reading missed economists’ expectations of 55.3 by a wide margin. The index has fallen 8 points below its post-2008 recession peak of 60.8 reached just last fall. The decline has largely coincided with the intensifying trade dispute with China. In the details, business production and new orders grew more slowly, while employment levels remained essentially flat. The index for production slid to 55.2 from 61.5. The employment gauge dropped to a five-year low of 50.4 — barely above the cutoff point that separates net hiring from net layoffs. The ISM indexes are compiled from a survey of executives who order raw materials and other supplies for their companies, and tend to rise or fall in tandem with the health of the economy.